03

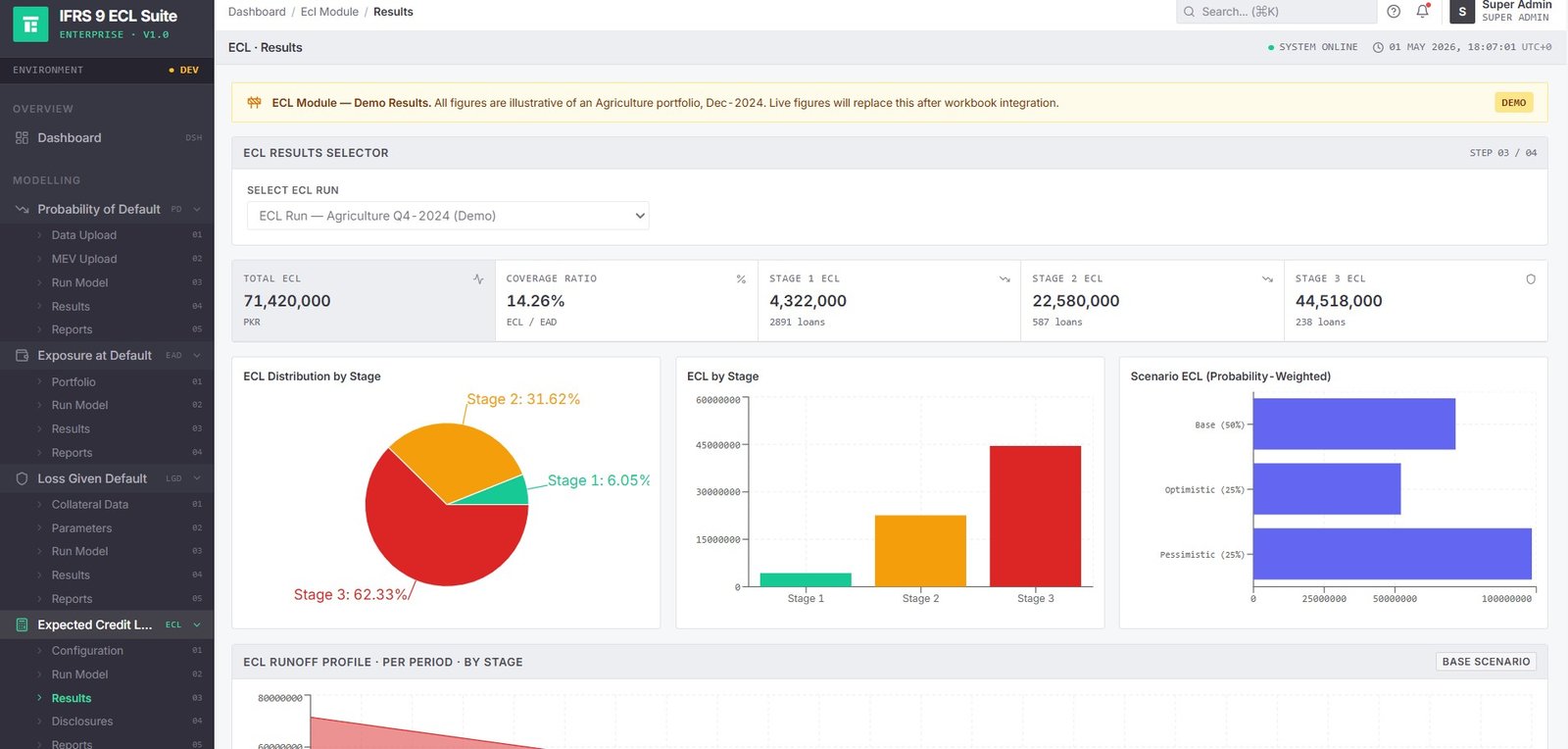

ECL Calculation

Scenario-Weighted ECL with Stage-Level Precision

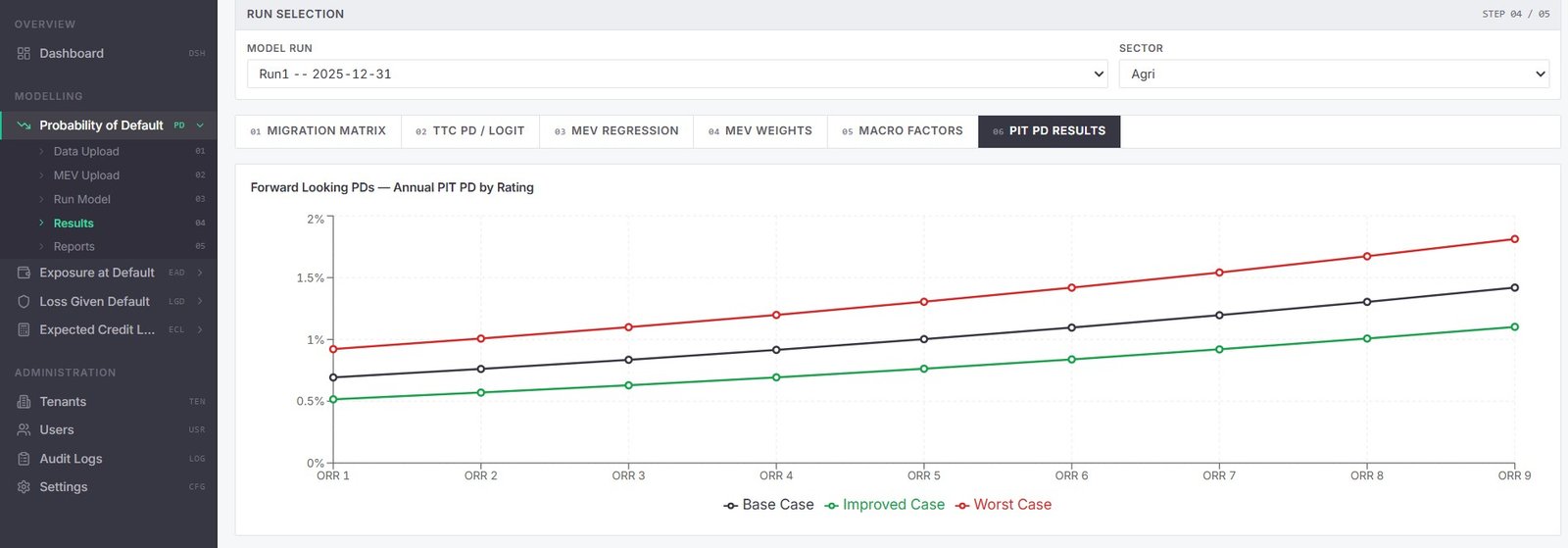

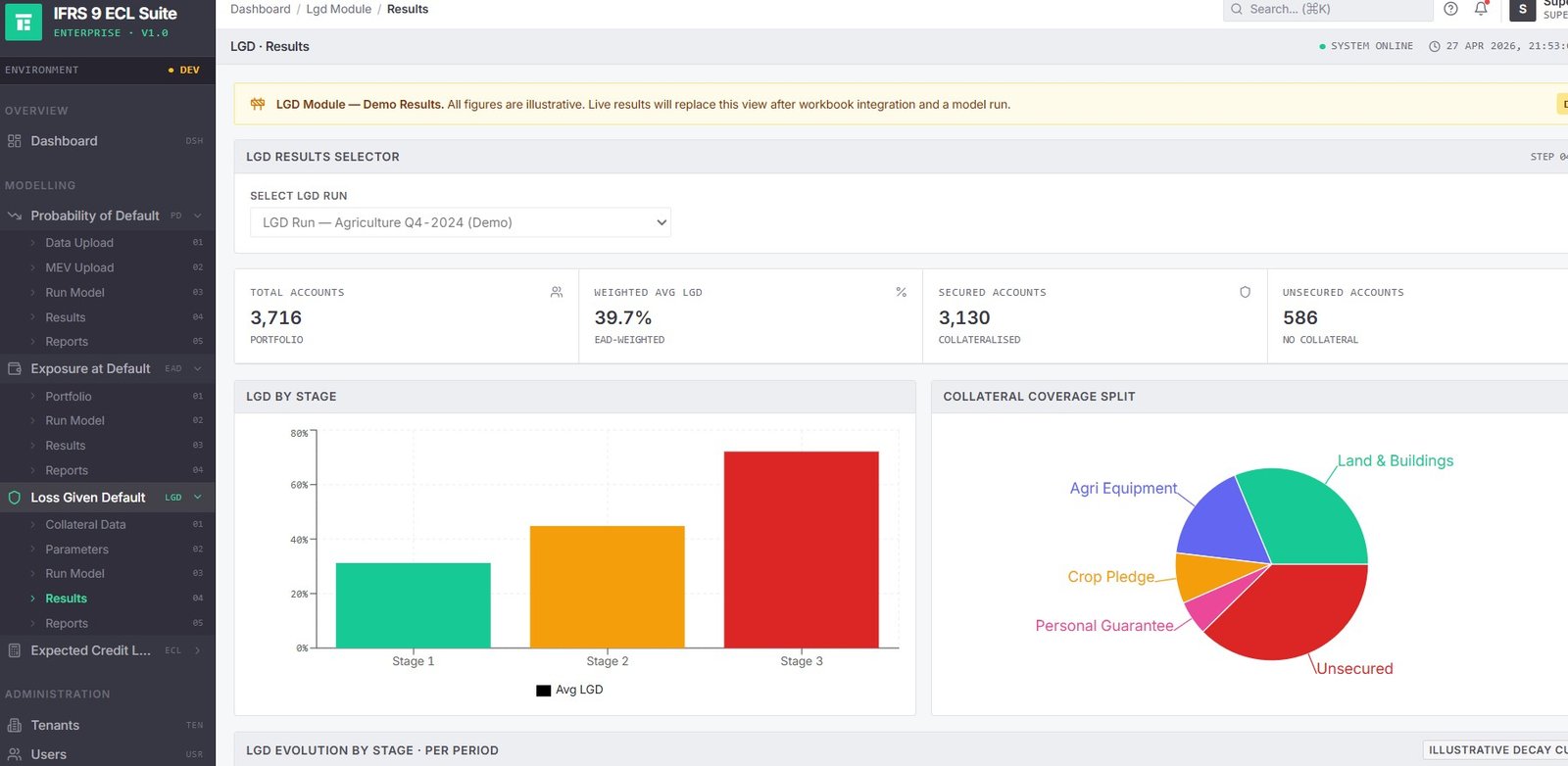

Combine calibrated PD, LGD, and EAD inputs to compute Expected Credit Loss across Stage 1, 2, and 3 — with probability-weighted macroeconomic scenario overlays, management adjustment capability, and period-to-period movement reconciliation.

- Total ECL computed and disaggregated across the full portfolio

- Stage-level ECL split: Stage 1 (12-month), Stage 2 & 3 (lifetime)

- Configurable scenario probability weights — Base, Optimistic, Pessimistic

- Coverage ratio monitoring with period-to-period movement reconciliation

- Provision waterfall from prior period with stage transfer tracking

- One-click export: journals, disclosures, movement tables